How Does Compound Interest Grow So Fast?

Exponential growth from interest on interest

Compound interest grows fast because each new interest payment gets added to the money that earns interest next time. The balance does not rise by the same number of dollars each year. It rises by a growing number of dollars because the base keeps getting larger.

Compound interest is one of the clearest real life examples of exponential growth. You start with a principal, which is the original amount of money. After one interest period, the interest is added to that principal. During the next period, interest is paid on the larger balance. That small change makes the growth speed up. A savings account, a loan, and a credit card balance can all use this pattern. The same math also appears in population growth, bacteria growth, and some models of technology use. In high school algebra, compound interest is usually written as $A=P(1+r)^t$. The multiplier $(1+r)$ tells how much the balance changes each period. A graph of that rule bends upward, not because magic is happening, but because the same percent is applied to a larger amount each time. You can explore related growth patterns with LivePhysics math tools after building the model by hand.

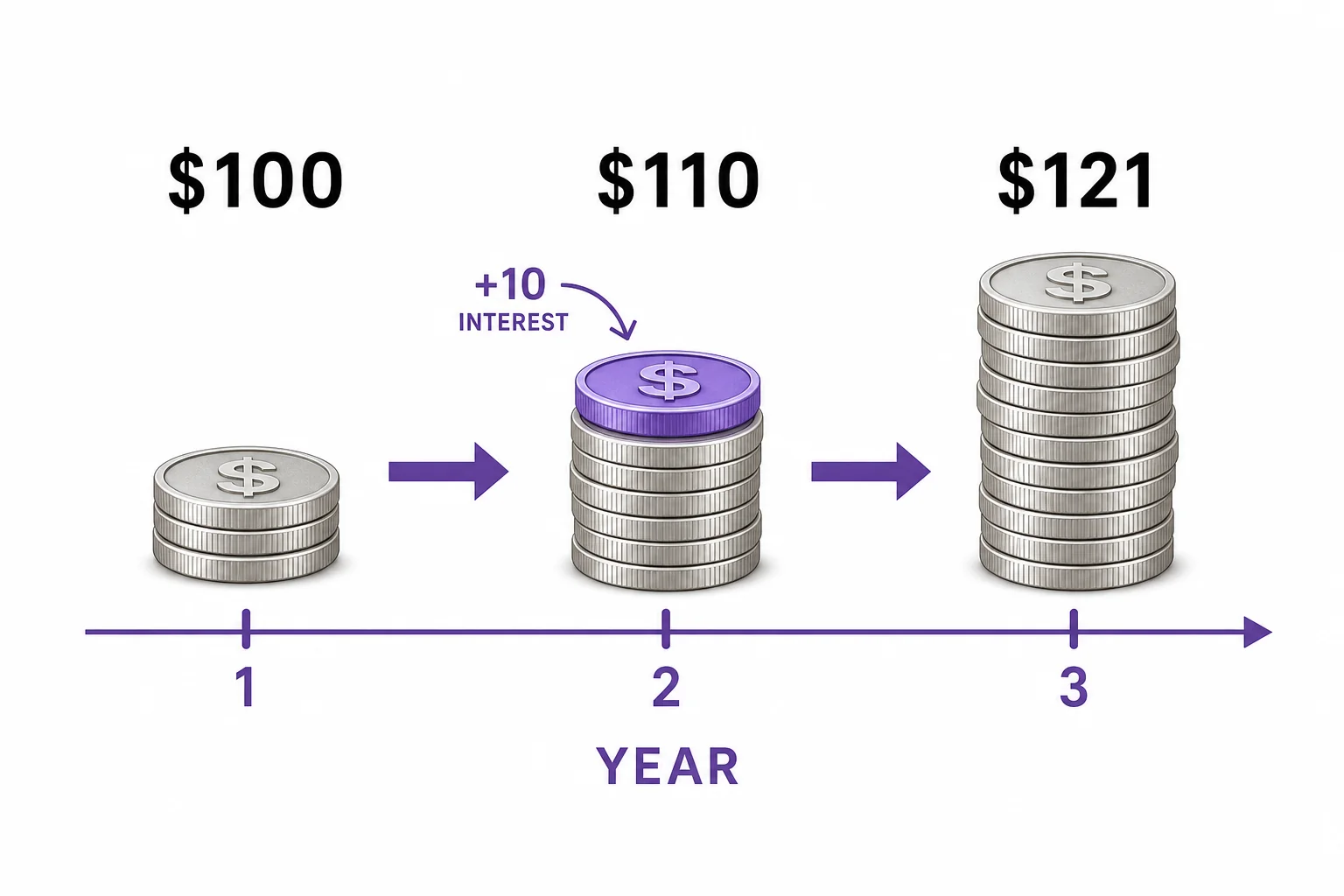

Principal Starts the Pattern

Compound interest starts when interest becomes part of the balance.

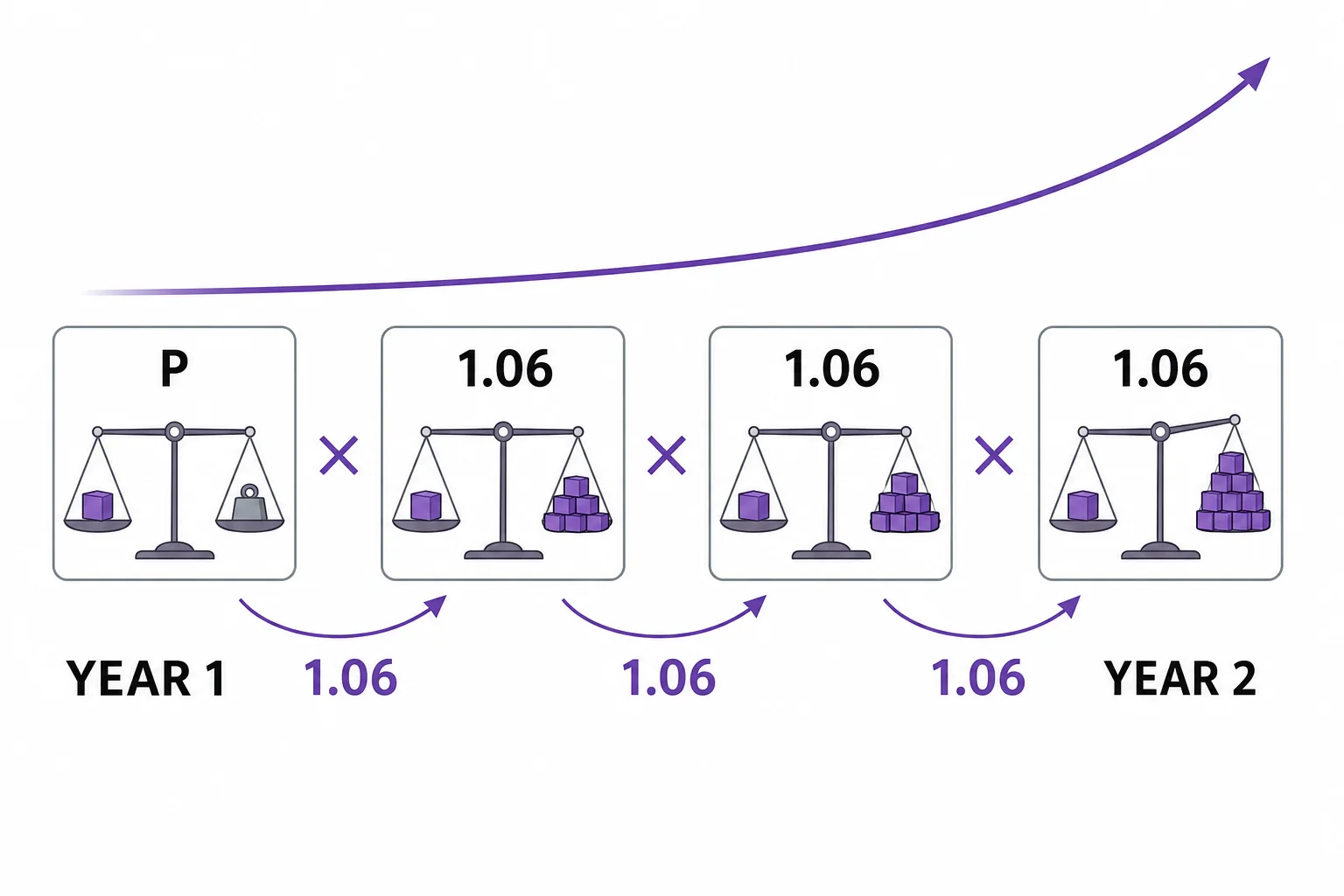

Growth by a Factor

Equal time steps use equal factors.

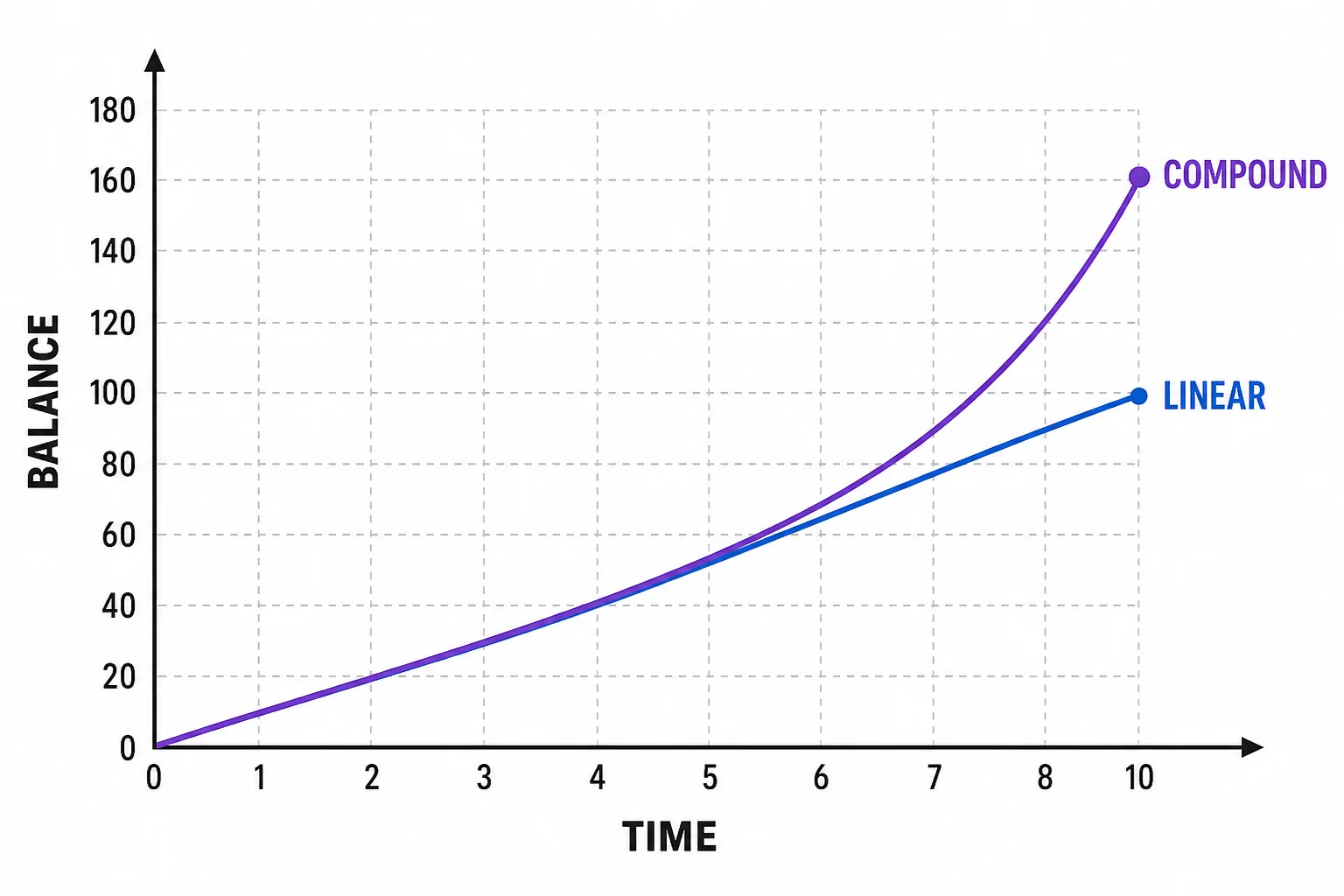

Why the Curve Bends Up

The percent can stay constant while the dollar change grows.

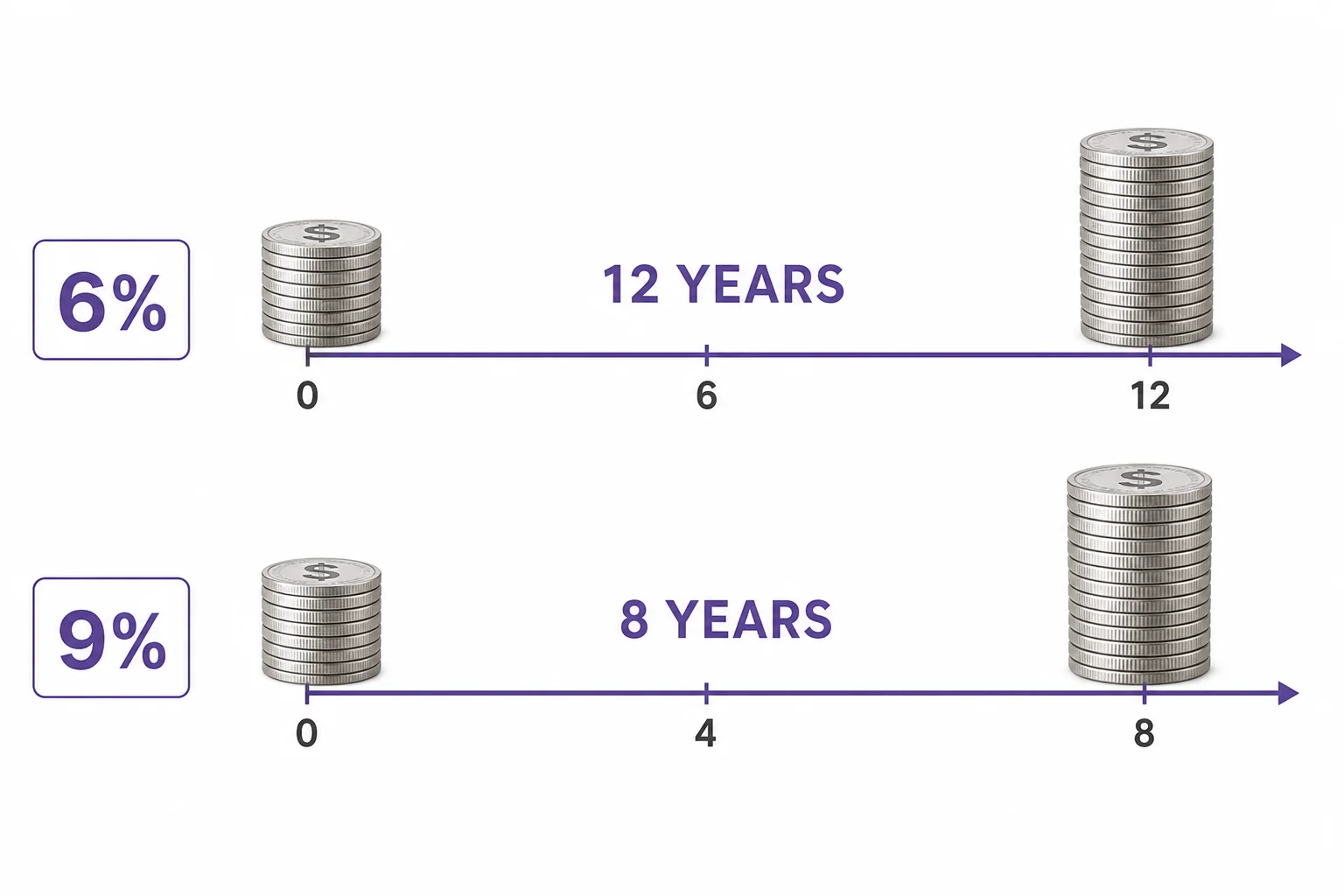

Doubling Time and the Rule of 72

Doubling time turns an exponential model into a quick mental estimate.

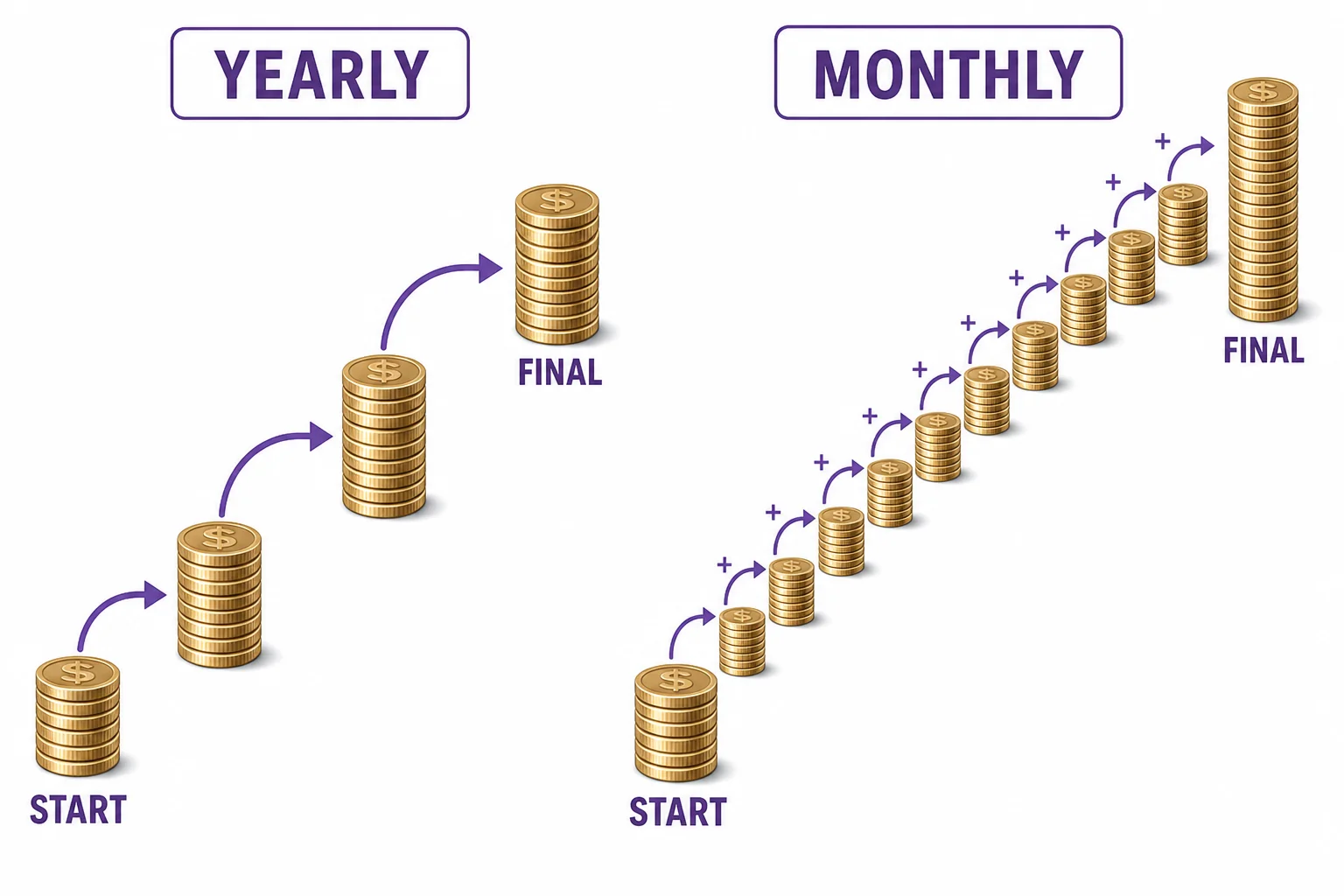

Compounding More Often

Compounding frequency changes how often the base is updated.

Vocabulary

- Principal

- The starting amount of money before interest is added.

- Interest

- Extra money earned or charged as a percent of a balance.

- Compound interest

- Interest calculated on the principal plus interest that has already been added.

- Exponential growth

- Growth by repeated multiplication by the same factor over equal time intervals.

- Doubling time

- The time it takes for a quantity to become twice as large.

- Rule of 72

- A quick estimate for doubling time found by dividing 72 by the annual percent rate.

In the Classroom

Build a compound table

20 minutes | Grades 9-12

Students start with a principal of 100 dollars and calculate yearly balances at 5 percent for 10 years. They compare the yearly dollar gains and explain why the gains increase.

Graph linear versus compound growth

30 minutes | Grades 9-12

Students graph simple interest and compound interest on the same axes. They identify which model has constant differences and which has constant ratios.

Test the rule of 72

25 minutes | Grades 10-12

Students choose several annual rates and estimate doubling time with the rule of 72. They then use the compound interest formula to check how close each estimate is.

Key Takeaways

- • Compound interest adds interest to the balance, so future interest is calculated on a larger amount.

- • A fixed percent increase is repeated multiplication, not repeated addition.

- • The formula $A=P(1+r)^t$ models yearly compounding when the rate is written as a decimal.

- • The rule of 72 estimates doubling time by dividing 72 by the annual percent rate.

- • More frequent compounding usually makes the final balance slightly larger.