Why Do Insurance Companies Always Win in the Long Run?

How averages make risk predictable

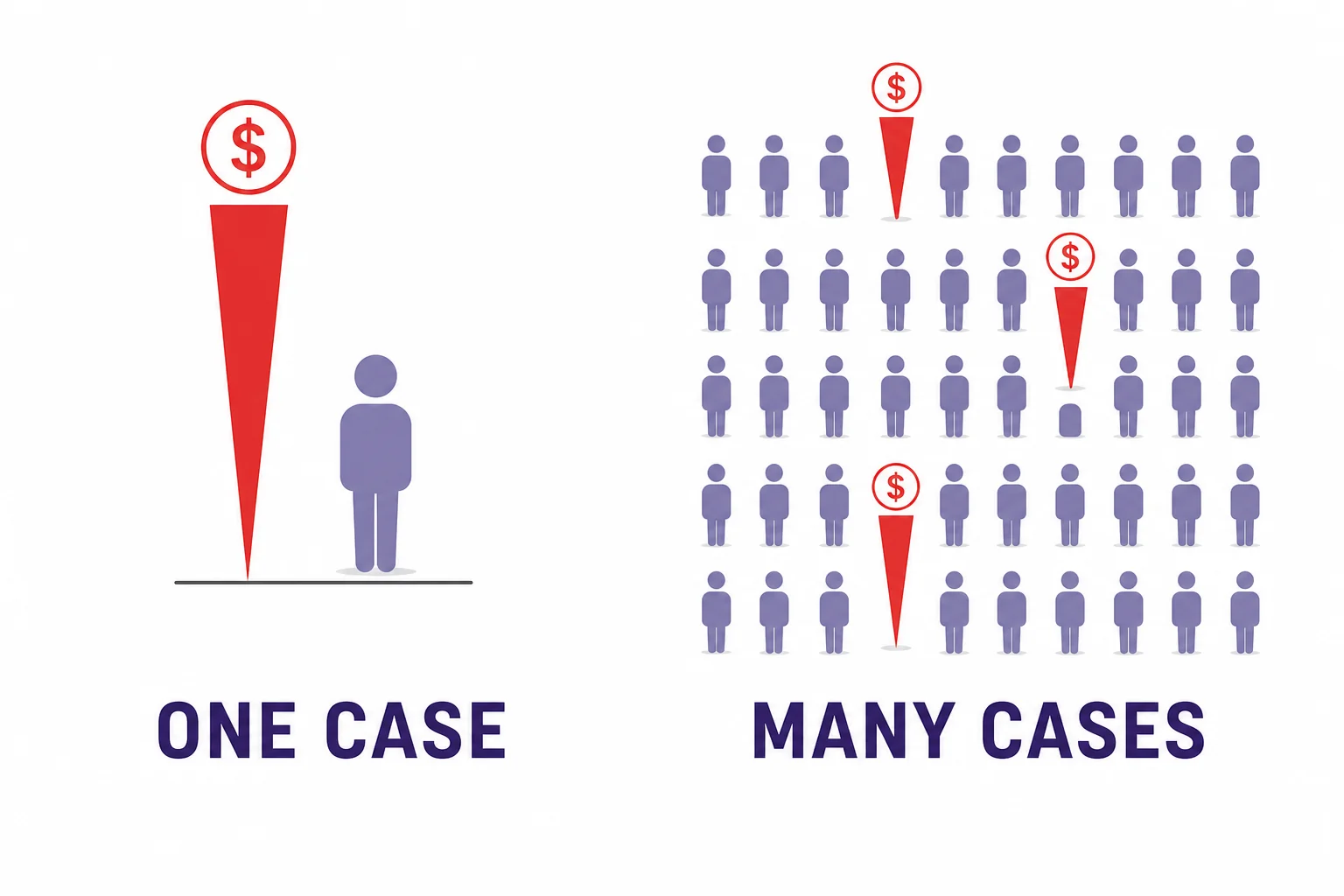

Insurance companies charge many people a little more than they expect to pay back in claims. One customer may have a huge loss, but thousands of customers spread out the surprises. Over many policies, the company’s average result gets close to its plan.

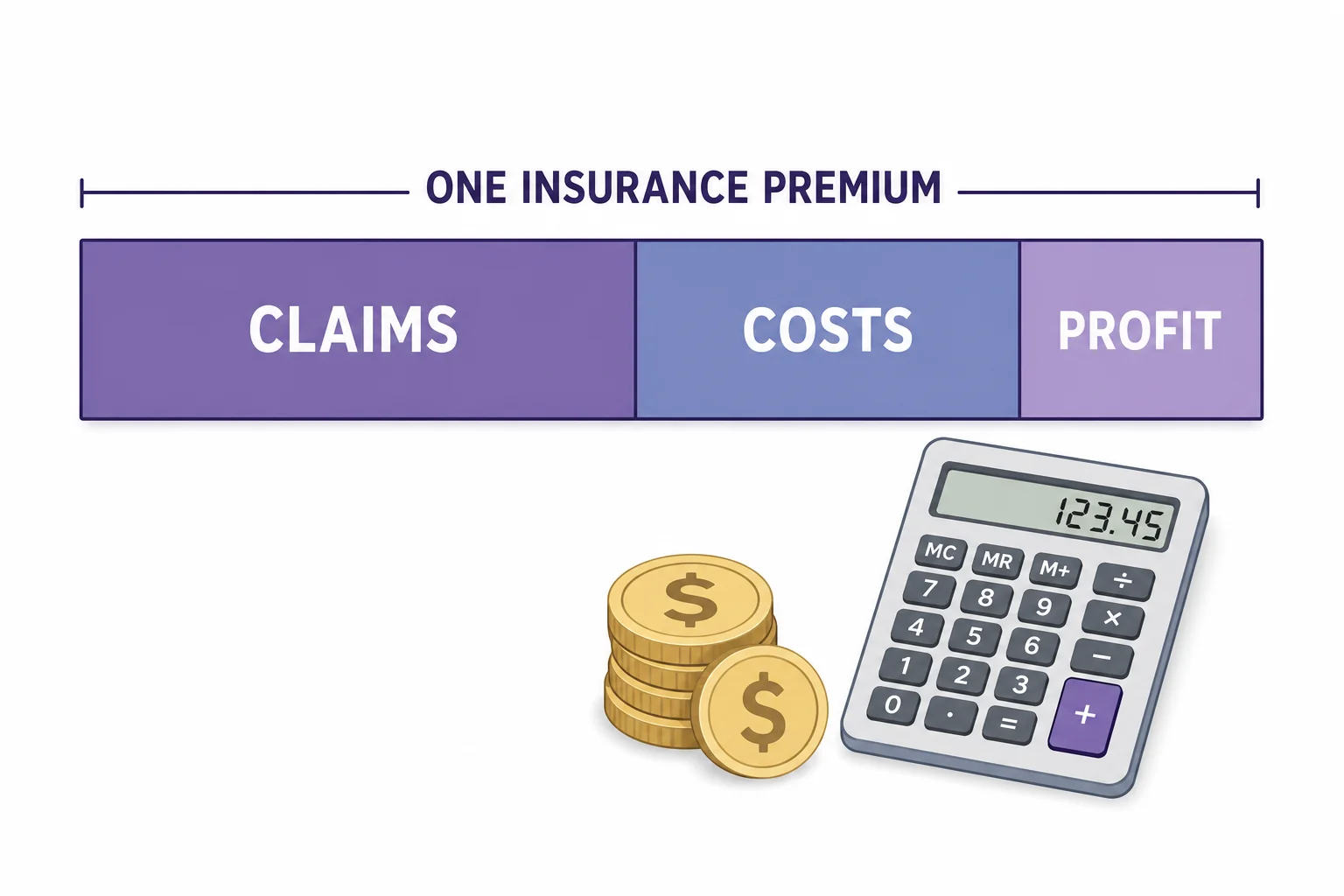

Insurance looks strange from one person’s view. You may pay for years and never file a claim. Another person may pay one premium and then receive a huge payout after a crash, fire, or medical emergency. That does not mean the company is guessing. It is using probability. For each type of policy, the company estimates how often losses happen and how large those losses tend to be. Then it sets a premium that is higher than the average payout it expects. That extra amount pays for employees, reserves, taxes, and profit. The key math idea is expected value, which is a weighted average of possible outcomes. If a loss of $\$10{,}000$ happens with probability $\frac{1}{100}$, the expected claim cost is $\$100$. A single customer can be unpredictable. A large group is much more stable.

The bet is not even

The company does not need every policy to be profitable.

One loss is noisy

Insurance math is about the group, not the single story.

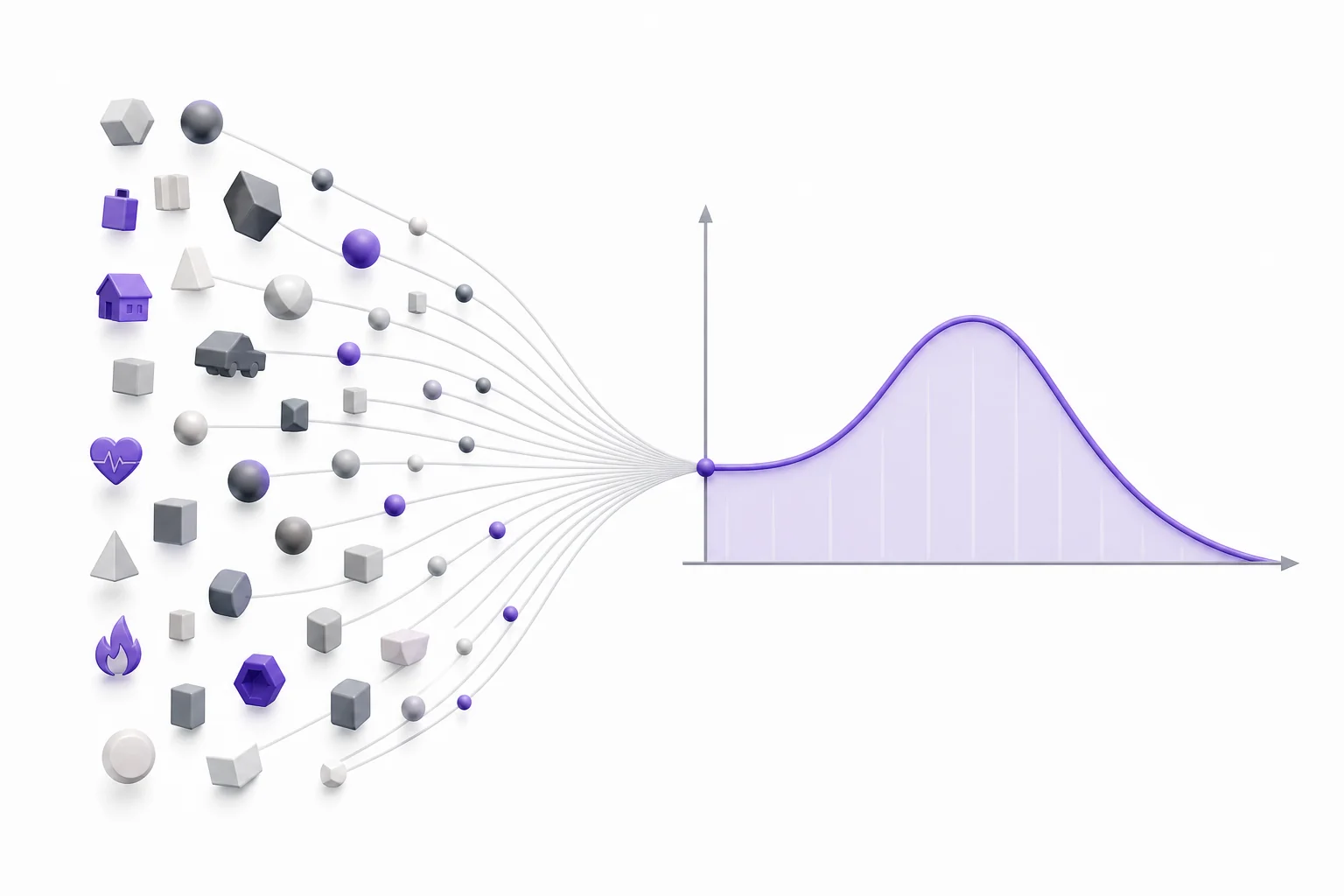

Large numbers smooth the average

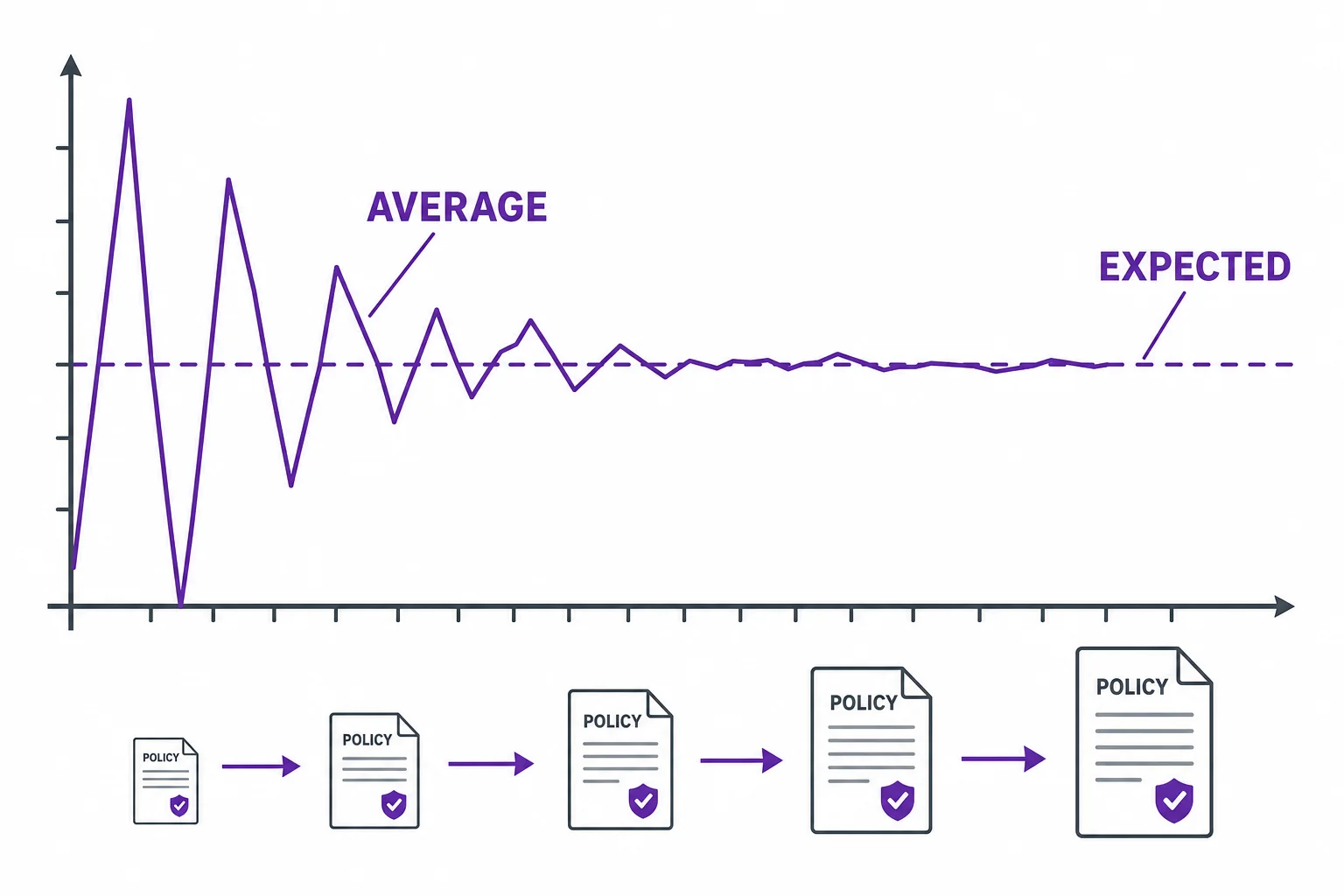

Big pools make averages more predictable.

Premiums include a safety margin

The margin protects the company from bad luck and bad estimates.

Winning is not guaranteed

Expected value is a plan, not a promise.

Vocabulary

- Expected value

- The long-run average result of a random process, found by weighting each outcome by its probability.

- Premium

- The amount a customer pays for an insurance policy.

- Claim

- A request for payment after a covered loss happens.

- Law of large numbers

- The rule that averages from many similar trials tend to get closer to the expected value.

- Risk pool

- A group of policyholders whose premiums and claims are combined.

- Reserve

- Money an insurer sets aside to pay future claims.

In the Classroom

Build a tiny insurance company

25 minutes | Grades 9-12

Students roll dice to simulate 100 drivers. A roll of 1 means a claim, and other rolls mean no claim. Students compare total claims with different premium prices.

Expected value pricing challenge

30 minutes | Grades 9-12

Groups receive loss amounts and probabilities for phone, car, or pet insurance. They compute expected claim cost, then add expenses and a risk margin to propose a premium.

Small pool versus large pool

40 minutes | Grades 9-12

Students simulate 10 policies, 100 policies, and 1,000 policies with a spreadsheet or random number generator. They graph the average loss per policy and connect the pattern to the law of large numbers.

Key Takeaways

- • Insurance companies use expected value to estimate average claim costs.

- • Premiums are set above expected claims to cover expenses, reserves, and profit.

- • One customer’s loss can be huge, but a large pool makes the average more stable.

- • The law of large numbers explains why many similar policies are easier to predict than one policy.

- • Insurers can still lose money if risks are priced badly or many claims happen together.